If you’re just starting to think about spreading your investments around the world but don’t know how to start, this is the place to be! In this blog post, we’re going to give you a beginner’s guide to investing in international markets. We’ll talk about the basic ideas, the plans you can use, and the things to watch out for when you’re putting your money into investments outside your own country. So, if you’re curious about Wall Street and investing internationally, keep reading!

The Context

Diversification and globalization are the keys to the future — Fujio Mitarai

We live in a world of growing interdependence. Trade and technology have made the world into a more connected network that relies on each other’s backs.

The term globalization attained popularity after the Cold War in the early 1990s, as a seemingly win-win agreement that has shaped our everyday contemporary life. Every consumer’s life has been seamlessly infused with trinkets and electronic circuits from China, software from the US, affordable shoes and apparel from Bangladesh, and high-quality medical equipment from Europe.

Trillions of dollars are involved in the scope of this global remedy. As of April 2021, the total market capitalization of all publicly traded firms worldwide was estimated to be a staggering $95 trillion. Also worth noting is that in the 1980s, this figure was just $2.5 trillion. Comparatively speaking, the NSE (India) market capitalization is only $3.2 trillion, while Wall Street (U.S.) is valued at $25 trillion.

International Diversification

By investing internationally, you can take advantage of investment opportunities that are not available locally. To further address the deliberation on Global Investing; serious investors must note that, international diversification helps reduce the concentration risk of investing in one region.

This approach in turn offers a potentially smoother ride over long holding periods. Institutions and High net worth investors (HNIs) have been playing this game for a long time. Due to outrageously high transaction costs and capital requirements, however, the average investor has shied away from this untapped world of opportunities. In addition to the previous factors, the Reserve Bank of India (RBI) aimed to restrict capital outflow, therefore before 2004, residents of India needed to obtain authorization from the RBI before sending money abroad.

The Reserve Bank Of India (RBI) was concerned that excessive outflow of money would destabilize the rupee and make it lose value. However, the RBI later acknowledged that unrestricted capital flows across international borders are crucial for economic expansion. As a result, the RBI implemented a new policy in 2004 to loosen the restriction on capital outflows. This new policy was called the Liberalized Remittance Scheme (LRS).

Under the LRS, individuals can send money across borders without seeking approval from the RBI. The LRS has made it easier for Indian residents to study abroad, travel, and make investments in other countries.

Under the Liberalised Remittance Scheme (LRS) of the RBI, a resident Indian individual can invest up to $2,50,000 per financial year in international markets. Furthermore, once an individual hits the maximum US $250,000 per year per individual limit, the individual must acquire special permission from the RBI.

Overall, flexible regulations, technological advancements, lower investment costs, and mob knowledge are leveling the playing field for Indian investors.

Imagine making an investment a decade ago in a company like Tesla (#TSLA), NVIDIA (#NVDA), or Adobe (#ADBE), and seeing an average Y-o-Y compounded annual growth rate of 30%.

The Fascination With Wall Street

There are about 21 stock exchanges globally that have a market capitalization of $1 trillion and above. But, ever wondered why international investing almost always resonates with U.S. stocks? It’s because international trade is a dollar-based economy. Besides, Wall Street has always provided foreign investors with a stable and welcoming market.

As a place to do business, the United States offers a predictable and regulated legal system, low taxes, outstanding infrastructure, and access to the world’s most lucrative, wealth-creating consumer market. Historically, the U.S. dollar gained its dominance post World War II. Before participating in the war, the U.S. served as the main supplier of weapons and goods to its allies. As most countries paid in gold, the U.S. owned the majority of the world’s gold reserves by the end of the war.

With almost no gold reserves, delegates from 44 Allied countries met in Bretton Wood, New Hampshire, in 1944 to come up with a system to manage foreign exchange that can fairly serve all countries. The delegation decided that the world’s currencies would no longer be linked to gold but could be pegged to the U.S. The arrangement came to be known as the Bretton Woods Agreement back in the day. Not to add that the U.S. dollar today is supported by the world’s most powerful military and more than 4,000 nuclear weapons.

As a result, the U.S. Dollar is regarded as one of the strongest and most stable currencies in the world, driving the global economy. But that’s not all, there are other factors as well that make Wall Street a preferred stock investment destination.

Laws and Creditworthiness

A sovereign credit rating is an independent assessment of the creditworthiness of a country or sovereign entity. Sovereign credit ratings can help investors understand the level of risk involved while investing in a particular country, including any political risk.

According to sovereign credit ratings, the United States is well-positioned relative to other international alternatives in terms of the level of risk involved. These ratings are provided by the three most influential rating agencies — Moody’s Services, Standard & Poor’s, and Fitch.

There are smaller agencies as well but their say is limited to influencing a few decisions finally taken by the 3 top agencies mentioned above.

These ratings are usually based on a combination of per capita income, GDP growth, inflation rate, external debt, economic development, and history of defaults among others. Along with the prime consideration of ratings, the procedure for investing in stock markets differs from country to country which confines many investors to venture beyond known and friendly territories.

Many nations score higher than the United States when it comes to creditworthiness, but their laws and regulations are not as favorable to investors as those in the United States.

For example, the U.K. has a good sovereign rating with a great outlook however the brokers there do not entertain retail investors if they are not a citizen of the U.K. On the contrary, Brazil, which is a developing economy has friendly laws for foreign investors but it suffers from political instability and corruption as per expert opinions.

Fitch affirms Brazil’s sovereign rating as BB- along with a negative outlook.

A BB- rating implies more vulnerability to default risk and more prone to economic changes.

From a comparison standpoint, the rating outlook for India is BBB- with a stable outlook. Though BBB is the lowest investment grade rating, it implies medium-class entities which are satisfactory at the moment.

Elements Of Taxation

When Indian investors decide to diversify the U.S. markets the most important element that is to be taken into account is taxes. Net returns here are of prime importance else the effort of taking so much pain is not worth your time.

If your investments resulted in a profit, you must pay taxes. Your Wall Street profits are taxable in India rather than in the U.S. There are primarily three components to it when an investor from India decides to explore options available in the U.S. markets.

1. Tax on Dividends

Everybody who enjoys dividends could find this knowledge useful. All dividends that you receive from your Wall Street stocks are taxed at 25% in the U.S. and further in India as per your tax slab with a peculiar exception.

All calculations work on the source dividend amount. While this seems a lot, in reality, it is lower than the standard rates that are applied to investments in other foreign countries.

This is because India and the U.S. have signed a pact known as the Double Taxation Avoidance Agreement (DTAA). This allows you to offset tax liability in India for the taxes that you have already paid in the U.S.

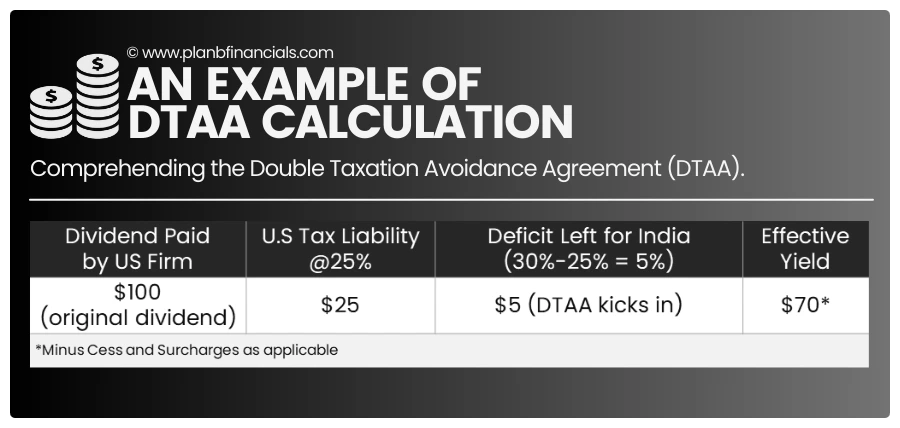

So, for a simple calculation, if you fall in a 30 percent tax bracket in India let’s say you received $100 divided.

This is what your tax liability will look like.

💬 25 percent flat deduction in the U.S

💬 Indian laws further dictate a 30 percent tax on the original dividend amount of $100

💬 But, you’ve already paid 25 percent of that in the U.S. and this is where DTAA kicks in

💬 Your actual liability becomes only the deficit of the domestic tax law, that is 5 percent of the original divided amount.

That’s 30% as levied by the Indian law minus 25% that already got deducted as per the U.S. law

💬 This means $100 (original dividend) – $25 (paid in the U.S.) – $5 (Deficit left for India) = $70 as an effective dividend yield.

2. Long-Term Capital Gains Tax

The gain from U.S. stocks is taxed at a long-term capital gains tax rate of 20% if the shares are held for longer than 24 months and the ETFs for more than 36 months.

For instance, if you sell a U.S. stock for $100 after holding it for 30 months, such a sale constitutes a long-term capital gain, and you will be liable to pay $20 in addition to any applicable cess and surcharges.

3. Short Term Capital Gains Tax

The gain from U.S. stocks is classified as regular income and taxed by your tax slabs if the shares are held for less than 24 months and the ETFs for less than 36 months, respectively.

For instance, after keeping the stock for 20 months, if you made a profit of $100, it would be considered a short-term capital gain, and you would be required to pay tax according to the income tax bracket you are in.

Conclusion

There are a total of 60 stock exchanges in the world and each of them has thousands of listed companies. The subjects we’ve just discussed, though, demonstrate how rational American stock market investing is to Indian investors.

The most dominant factors that support this idea are:

🖱 The dollar dominates the world economy

🖱 The U.S. has investor-friendly laws

🖱 The U.S. has a large consumer base

🖱 The U.S. houses some of the best companies in the world

🖱 The sovereign credit rating of the country boosts investor confidence

Because of this, investing in Wall Street is a wise choice if you wish to diversify your portfolio outside of the Indian subcontinent. If you want to learn how to invest in the U.S. markets, watch out for our next piece.

🔔 Investing is expensive, but leaving comments on this blog is free!