When you’re spending more money than you’re earning, saving becomes really tough. Let’s talk about some smart ways to save money that can help you have more to invest in your future. Saving money means finding ways to keep more of the money you earn, so you can use it for things that are important to you, like investing for your goals.

The Context

Spend less today and you’ll have more money tomorrow — PlanB

Hard-earned money can often feel like sand in our fists; the more we attempt to grasp it tightly, the more it eludes us.

Saving money is a discipline that needs to be mastered; you don’t need to be a quantum physicist to grasp this.

Throughout our investing journey, we have come across many people lamenting the fact that they never have enough money to invest, or simply say, “put money to work.” This may account for the statistic that 30% of Indians will never invest in their lifetimes.

One-third of Indians live paycheck to paycheck, according to a survey on spending habits by “www.dealsunny.com”

33 percent of our population is therefore just one paycheck away from financial ruin!

To add to the gloominess of the situation, 50% of Indians are solely responsible for providing for their families, leaving their dependents exposed as well.

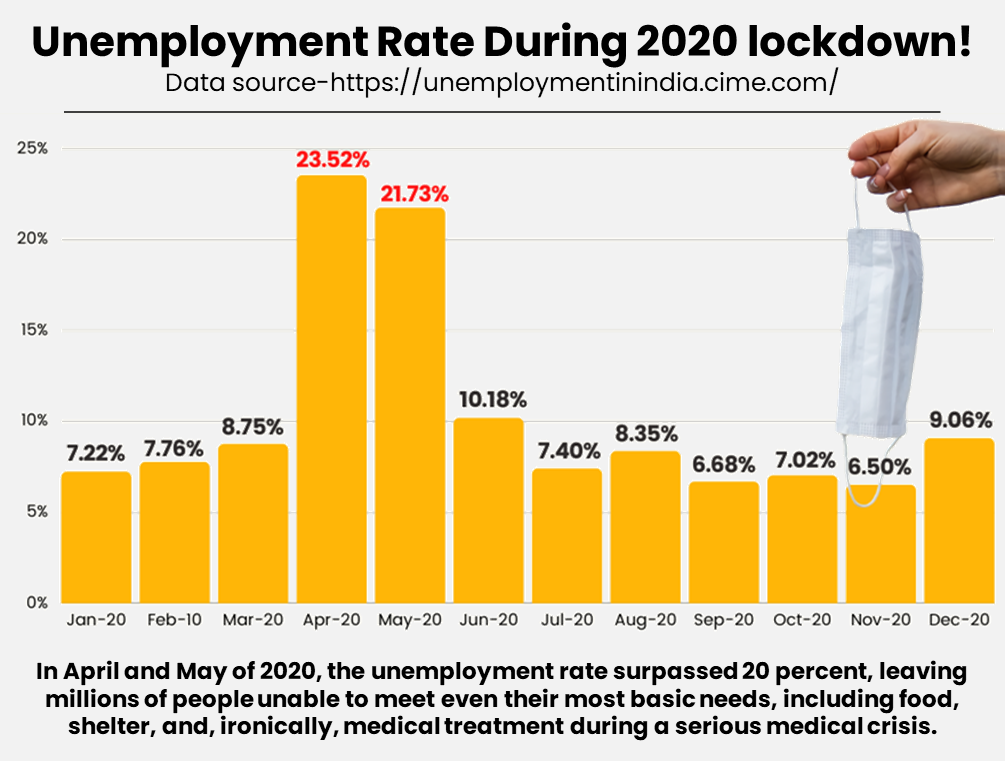

The results are worrying, and the 2020 COVID-19 aftermath served to confirm this once again.

This became especially clear in April-May of 2020 when India’s labor market was severely stressed, primarily as a result of declining employment rates in rural areas and relatively low employment rates in urban areas.

In both of these months, the unemployment rate exceeded 20 percent, leaving millions of households unable to meet even their most basic needs, including food, shelter, and strangely, basic medical treatment during a serious medical crisis.

Did you ever think about whether you have the financial resources necessary to survive in a crisis-like circumstance, even though you may be comfortably meeting all of your current obligations or affording that great lifestyle year after year? An ordinary man must develop a counter-strategy to overcome the odds because employees are still often forced out of organizations.

The only way to accomplish this is by patiently saving and investing the extra cash. The good times will multiply your money, strengthening your capacity for risk-taking, and the difficult times will give you the sense to make the right choices and get through them.

This thorough advice can undoubtedly help you get started in the right manner even if you are not one of those 3 Indians who are living paycheck to paycheck as mentioned above. For the best outcomes, feel free to follow them in order.

Track Your Spending

A small leak can sink a great ship

The first step in scouting your field of battle is keeping track of where your money is going. Money is funny in that there is never enough of it.

Our lifestyles become more luxurious; our toys get bigger and more expensive as we earn more money. Do you recall how we began when we were little with our pocket money, eh? Previously, tiny cash seemed like a fortune; today, it sounds like pennies! – The term “lifestyle inflation” refers to this.

There is no guilt in keeping track of every penny of your spending.

Many individuals consider this to be a cheap or insignificant action because they fall victim to continuity bias, which is the belief that the flow of money will always be the same. This kind of misconception typically comes to an end when the individuals recognize that the roles have been reversed and that the once-servant-like cash flow now exerts complete authority over their lives.

Using a pen and paper or even an MS Excel workbook is an antiquated but great method of keeping track of your finances. This is a great way to start and will show you how each dollar has moved specifically.

Try out our NO COST introductory Excel course to get started.

A more contemporary method is to use one of the myriad money-tracking smartphone apps that are available. Some examples are — ET Money, Walnut, Monefy, Andromoney, Wallet, Monthly Budget Tracker, etc.

According to our analysis, these are some well-known apps with potentially smaller drawbacks. By utilizing interactive outputs, fundamental statistics, and some stunning tips, they assist you in tracking and analyzing spending. The majority of these apps can automatically read your phone’s spending-related messages and identify them under different buckets.

In addition, they do provide you with the choice of making manual inputs, particularly for any cash transactions. Please be advised that in exchange for a free service, they collect information on consumer spending habits to target adverts and products. You could decide whether to hear about new products occasionally, although we don’t mind.

Make A Budget

After keeping track of your expenditures, you can see exactly where your money is going. Now is the time to establish a monthly spending plan.

Fixed expenses and variable expenses are the two main types of spending that make up a monthly budget.

What Are Fixed Expenses?

These are the expenses that are constant in nature and do not vary much from month to month Utility payments like internet, cell phone, water, streaming subscriptions, residential maintenance, and or car loans and home loan EMIs are a couple of examples.

Look for strategies to reduce leaks that are draining your finances if your spending analysis indicates that you are spending too much on fixed expenses. This could be a costly data plan that never exceeds the extra data limit, a streaming service that you don’t have time to use, the loan payment for that second automobile, or something else.

What Are Variable Expenses?

Variable costs are those that vary from month to month based on your consumption habits. Examples include buying groceries, eating out, using credit cards, buying coffee every day, going out to lunch, and making pointless purchases on e-commerce sites merely because they are giving a deal.

Look through the last three to six months’ worth of expenditure to determine which categories are stable and which ones are changing it clearly identifies the variable expenses in your budget. Your variable expenses are the categories that change, and they can quickly push you over your monthly spending limit. You can feel more in control of your finances by developing a rigorous budgeting process that accounts for variable costs.

Take Control

The key here is to be economical without being cheap.

It would now be simple for you to take control of your spending habits once you’ve created your budget. You should consciously reduce your spending if you realize that your expenses are too high and it’s becoming difficult for you to invest and save money. The initial area of concentration should preferably be the variable expenses, even though it’s not advised to reduce fixed costs until your position is worrying.

Here are a few practical strategies for reducing variable costs:

≡ Delay or space out events and outings to reduce the amount you spend on outside entertainment.

≡ Instead of drinking that costly scotch all the time, consider finding less expensive forms of entertainment. A good cup of home-brewed coffee with your loved ones can also assist in producing the same amount of relaxation.

≡ Embrace the Jay-Z rule before engaging in excessive shopping. The golden rule says — If you can’t buy it twice, you can’t afford it!

≡ Develop the gene for delayed gratification. Place your next temptation in your shopping basket when making an online purchase, but don’t check out right away.

≡ Ignore the toxic wealth that surrounds you since it frequently causes irrationality, jealousy, and fruitless temptations.

≡ For the majority of your purchases, try to use cash or cash equivalents. Paying large sums of money as wads is never enjoyable.

Pay Yourself First

It’s a straightforward idea that’s frequently misunderstood.

If you believe that spending money from your paycheck on necessities like bills and luxuries qualifies as “paying yourself,” you are misinformed.

The money you pay for bills goes to businesses and collectors, not to you!

Paying yourself means setting aside a predetermined sum for your investments and savings, which will continue to grow through profits and compound interest. This is accomplished by automatically deducting a set amount for savings from each paycheck as soon as it hits your salary account.

You might start by adhering to the straightforward 50-20-30 rule of thumb to achieve this.

According to this rule:

≡ 50 percent of your income should be allocated to living expenses, such as groceries,

≡ 20 percent should be saved for your short-, medium-, and long-term goals, and

≡ 30 percent should be allocated to lifestyle expenses, such as entertainment, dining out, travel, and other seductions.

Set Goals And Priorities

There is a significant difference between sailing away with predetermined coordinates and drifting in the water.

You are merely going with the flow if you have no idea where you are going. The problem with drifting is that you’ll never be sure whether you’re moving ahead or backward. It’s crucial to plan out your savings goals before you begin. Priorities and objectives should always be established before investing your savings.

Your objective can be to satisfy a short-term need, a medium-term expense that is scheduled in a few years, or a long-term objective like creating a nest egg for retirement.

It is possible to prioritize numerous goals using sane logic. For instance, it might be a bad idea to focus all of your savings and income on your child’s college education while neglecting your retirement needs.

While your child, who is still young, may be eligible for and be able to repay an education loan, no financial institution will lend you money to sustain your retirement lifestyle if you do not have an active source of income or other means to settle that obligation.

Automate Your Bill Payments

This is a crucial trick to clear the mind of the extra junk that hangs around. Eliminating unintentional late payment fees, not only helps save a tonne of time, but also a tonne of money. Automate all of your recurring costs, including life insurance premiums and, most crucially, fixed expenses like phone, internet, credit card payments, and monthly investment plans.

You can set a credit limit for the transfers and add these merchants as a biller once to your payroll account. As soon as the bills are generated, money will be promptly credited from your account. By doing this, you can guarantee that you always have enough money in your account to cover short-term debts, and as an added benefit, not skipping utility payments will improve your credit/CIBIL scores over time.

Manage The Spontaneous Influx

The most common error is relying on a future inflow of funds, such as gifts, bonuses, dividends, or anticipated returns from fixed deposit maturities. As a result, money that you don’t yet have in your bank account is spent in advance.

Never plan future income into your current budget; instead, strive to steer it toward your investments.

Set Up An Emergency Fund

An emergency fund is not an investment!

A highly liquid reserve of cash that is always available and set aside for emergencies is known as an emergency fund.

When you begin to take charge of your finances, you should start by building this basket.

- If you have regular work, your emergency fund should ideally be three months’ worth of costs (in a stable & debt-free organization)

- If you work contract or seasonal jobs, six months’ worth of expenses

- In the case that you are self-employed, a year’s worth of expenses

In addition to providing you with a sound night’s sleep, your emergency fund should also enhance your capacity for taking calculated risks.

Imagine the self-assurance and ease you will exude when negotiating better employment terms or when you finally decide to invest in risky assets like stocks.

Focus On Building Your Portfolio

Remember that investing and saving are two different things. We’re going to assume that you don’t have your savings stashed away in a coffee can!

Savings typically refer to keeping money in a fixed-income investment with low returns that (to an extent) protect your wealth against inflation while also serving as an emergency fund (when needed). Certain sums, such as the one designated for an emergency fund, ought to always be kept in fixed-income investments.

However, the surplus should be fairly allocated and invested across a range of asset classes. This is referred to as building a functional portfolio. The main goal of putting together a portfolio of investments is to grow your money faster than inflation while still earning respectable returns.

You are only losing money on an investment if it does not produce a return that exceeds the current rate of inflation.

It takes careful planning and selecting the ideal ratio of the high, medium, and low-risk asset classes, including bonds, equities, metals (like gold), and real estate, to build an investment portfolio, which may be tedious, and painful, but rewarding process.

For help determining the “appropriate mix of assets,” please seek the advice of a professional advisor as this will depend on your objectives, personal capabilities, investing horizon, and risk tolerance.

Follow The Discipline

Talk doesn’t cook rice – An old Chinese proverb

Learning something new and not putting it into practice afterward is like talking trash that never comes to fruition. Humans do not possess discipline as a natural quality; it is an acquired skill. The first step in implementing a discipline is to admit that there is (or perhaps even is) a problem.

The majority of people lack discipline because they frequently avoid challenging or uncomfortable situations. Accept the truth, begin slowly, and then step up your game to seize control of what is rightfully yours.

We genuinely hope that the knowledge we have provided will enable you to succeed in the financial sphere of life.

Frequently Asked Questions (FAQs)

1. Why is it important to track my spending?

Tracking your spending helps you understand where your money is going and identify areas where you can cut back. By keeping a close eye on your expenses, you can make learned decisions about your finances and prioritize your spending accordingly.

2. How do I create a budget that works for me?

Creating a budget involves categorizing your expenses into fixed and variable categories and setting limits for each. By analyzing your spending habits and identifying areas where you can save, you can establish a budget that helps you achieve your financial goals.

3. How can I reduce my expenses without sacrificing my lifestyle?

Reducing expenses doesn’t have to mean sacrificing the things you enjoy. By being mindful of your spending habits and making small adjustments, such as cutting back on unnecessary purchases or finding cheaper alternatives, you can save money without drastically changing your lifestyle.

4. What does it mean to “pay myself first,” and why is it important?

Paying yourself first involves setting aside a portion of your income for savings or investments before paying your bills or other expenses. This ensures that you prioritize your financial goals and build wealth over time, rather than spending all of your money and saving whatever is left over.

5. How can I start building an emergency fund?

Building an emergency fund involves setting aside enough money to cover several months’ worth of expenses in case of unexpected financial setbacks, such as job loss or medical emergencies. By automating your savings and prioritizing building your emergency fund, you can create financial safety for yourself and your family.

🔔 Investing is expensive, but leaving comments on this blog is free!

3 Comments

Unemployment is still a big problem in India. Rich is getting richer and the poor are struggling to make both ends meet.

‘Do you know how many athletes go broke three years after they stop playing? I want to help them hold on to their money. I mean, I know about budgets’ -JayZ

A wonderful quote from a great entrepreneur. Thanks for sharing Geetanjali 🚀