In every market system, prices carry a treasure trove of data. Yet, deciphering their implications poses a challenge for novice investors. Let’s dive into the significance of one of the most widely used metrics by investors – the PE Ratio.

The Context

Finding intrinsic value using profit models is one of the most popular and simple strategies used by many people in this sea of numbers.

One such statistic that’s regularly utilized by innumerable investors to value a business is the P/E Ratio or Price Earnings ratio.

Price to Earnings appears to provide a reasonable idea of whether a stock is overvalued or undervalued against its competitors. As a general rule of thumb, a low P/E ratio may indicate that a stock is trading at a discount, while a high P/E ratio suggests that a firm has a high valuation.

The P & E of a stock tells us how many times an investor appreciates the stock.

Simply put, P/E reveals how many monetary units an investor is prepared to sacrifice for one monetary unit of profit generated by a company that issued the share. This readiness is determined by how much an investor, a group of investors, or the market is willing to pay now for a stock based on its historical or projected earnings.

The price or willingness to pay is a hazy concoction of consensus generated from numerous assumptions made by experts, trained/untrained retailers, and multitudes of speculators participating in the markets.

As a result, both the process of reaching a consensus and the stock’s P/E are very dynamic. While this appears to be legitimate on paper, the fundamental issues with P/E stem from its assumptions. All profit models concentrate on short-term time horizons, which can only go out for two to three years at most.

Purchasing stocks solely based on P/E may prove to be a costly error if you are a value investor with a prospect that extends beyond two years.

The PE Paradox

Price Earning ratios come in a variety of forms, including Historical, Forward, Sharpe, Regression, Shiller, and Normal P/E ratios. The one, however, that is listed on the stock exchange is known as TTM P/E. (TTM stands for trailing twelve months).

TTM P/E is the current share price divided by the sum of the last 4 quarterly EPS numbers. Because corporations report their quarterly financial data, including EPS. It is relatively simple to compute TTM P/E.

For instance, company A’s share price is ₹100 and its aggregate earnings per share over the previous four quarters are ₹10.

Then P/E = 100/10 = 10.

Another frequently used variation of P/E is called forward P/E. Forward PE is the current share price divided by the projected EPS over the next 4 quarters.

Usually, neither free data providers nor stock market websites have access to this.

Calculating forward PE requires professional expertise and skill investments because it involves forecasting sales, margins, P&L, and most importantly the “EPS” to be used as a denominator. Based on the direction provided by the firm management as well as their expertise and research, stock analysts professionally forecast future earnings and PE ratios.

Lower projected earnings are indicated if the forward P/E ratio is greater than the TTM P/E ratio.

The challenge of interpreting P/E ratios

Understanding Price to Earnings is highly reliant on its sectors and peers. Some stocks always trade at higher P/E ratios, just like some industries, including FMCG and pharmaceuticals, do. Due to a persistent display of rapid growth, the P/E of such stocks and sectors tends to always float at higher levels.

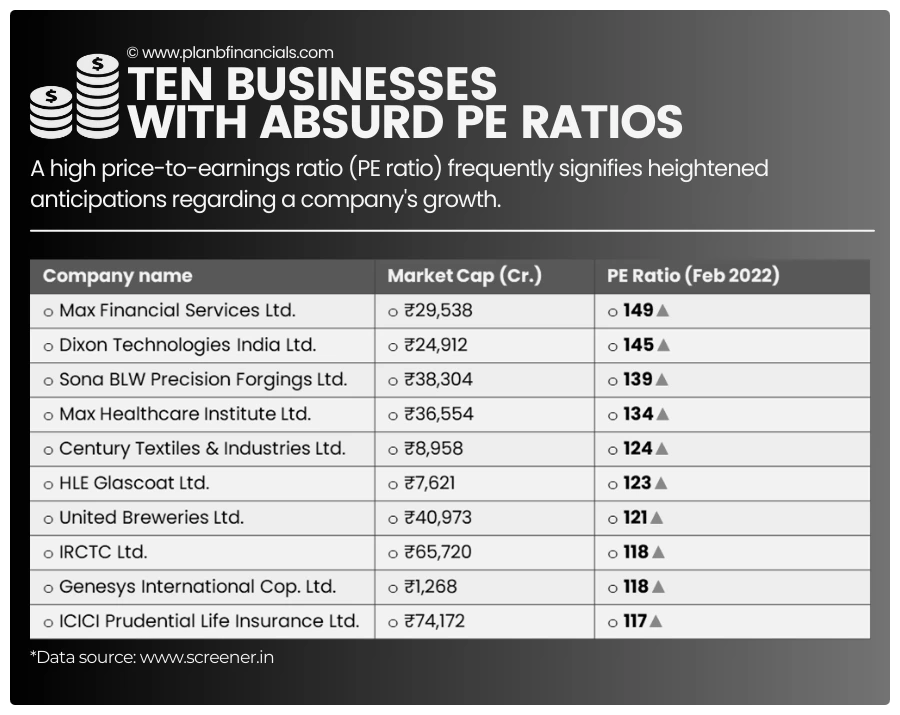

For example, companies like Page Industries (#PAGEIND), Titan Company (#TITAN), Honeywell Automation (#HONAUT) & Pidilite (#PIDILITIND) are all selling at a P/E of more than 99 as of February 2022.

According to PE reasoning, this indicates that if you bought these stocks today, you will have earned enough money to recoup your whole investment after 99 years. All future profits from that investment are gains only from that point and beyond.

How likely is it that you’ll live for the next 99 years and a few more to reap the benefits of any prospective prize that may follow? There’s a catch, though. The prices of all the aforementioned businesses may continue to rise in lockstep with their earnings for years to come. It’s more like a steady balance between the numerator (The Price or P) and the denominator (the EPS or the E).

Their Price to Earnings might never come down to a level that fits into a good P/E logic and these stocks may very well be selling cheap now at a P/E of 99!

For instance, Page Industries (#PAGEIND) has delivered a CAGR of 33% over the past ten years; hence, technically, a stock like PAGE Industries can still command a P/E multiple of 330, if the business maintains its earnings in the years to come.

With a low PE stock, this dilemma becomes more complex.

Low PE may be an indication of an inexpensive company according to the Price to Earnings theory, but it may also be a symptom of mediocre performance both now and in the future, making it a bad investment.

The unknown factors in price-to-earnings

☑ PE doesn’t consider the Debt conditions

☑ The management may always manipulate revenue

☑ PE does not take cash generation into account

☑ PE presents difficulty in assessing the income quality

☑ It’s a comparative approach

☑ The PE ratio is very volatile in the short-term

☑ It’s too subjective (Growth projections, EPS assumptions, etc.)

☑ PE reacts quickly to transient market-skewed events like mergers, acquisitions, and anomalous financial results, among others

There’s an imperfection

Many websites do not accurately update their data, which is another significant flaw that many investors frequently ignore. These websites find it more convenient to automate their procedure due to a large amount of publicly traded equities.

Most free stock market websites calculate EPS (the E of P/E ratio) by dividing profit after tax (PAT) by the number of shares (as the denominator) to calculate EPS. Due to an increase in the number of shares (the denominator) that the company has issued, a corporation that generates significant profits occasionally will have low EPS. The number of shares may rise as a result of bonuses, splits, new issues, or the exercise of stock options.

PAT (the numerator) is also influenced by many reasons such as the sale of an asset or other income. If you do decide to examine P/E, it is always preferable to rely on your EPS calculations by discounting for such anomalies from the actual firm balance sheet and calculating your own P/E ratio.

Conclusion

Over the past 20 years, the P/E ratios of the NIFTY 50 (India) and S&P 500 (the US) have averaged about 20 and 25, respectively. While these averages can help us determine if a stock or the market as a whole is overvalued or undervalued, they cannot be relied upon as a dependable guide to finding fantastic deals on undervalued stocks.

Although the P/E ratio appears to be favorable on the surface, it has serious drawbacks. If you are an investor who is just using P/E ratios to put together those purchase and sale choices, we strongly advise you to start referring to other underlying indicators as well to create a compelling argument.

You can also sign up for our carefully vetted programs if you think this post raises too many nerdy red flags about your choices.

These tailored courses cover fundamental methods for valuing investments including growth valuation, dividend discount, discounted cash flow, and comparative valuation (including hands-on calculators and free data sources).

Note – The mention of any stocks or businesses in this article is just for educational purposes and in no way constitutes investment advice of any sort.

Frequently Asked Questions (FAQs)

🔔 Investing is expensive, but leaving comments on this blog is free!

2 Comments

Incredible to see how a complicated metric is clarified with such modesty. Can you share more writings on stock market metrics!

Sure, thank you for your feedback ✨