Ever heard of portfolio rebalancing? It’s like setting rules for yourself to make sure you don’t take unnecessary risks when you’re investing. In this article, we’ll dive into the ins and outs of this strategy and share some handy tips to make it work for you.

The Context

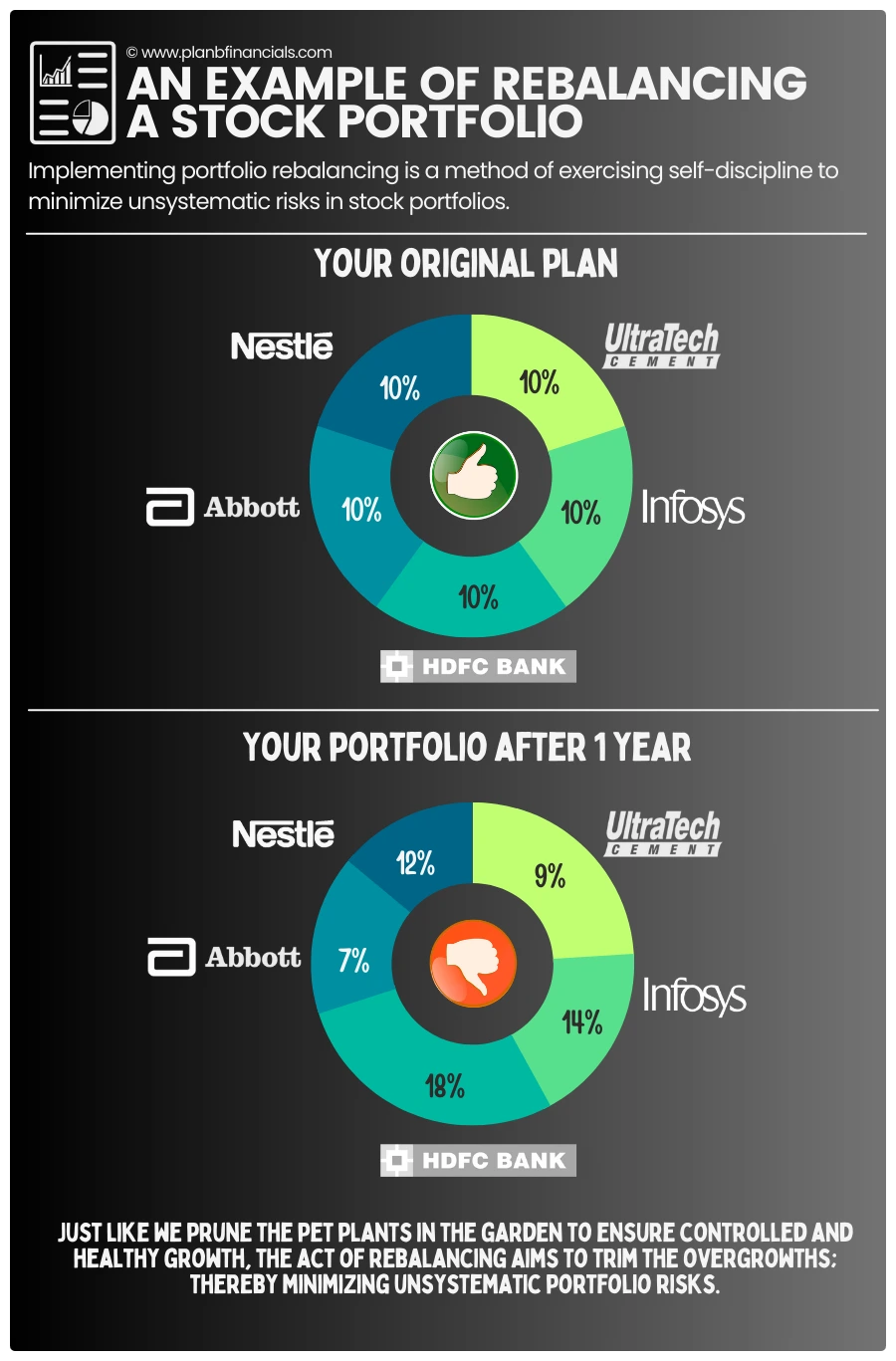

Rebalancing your stock portfolio is a method of enforcing self-discipline that helps in reducing unsystematic risk — PlanB

Rebalancing is a strategy to lower portfolio volatility while keeping the asset allocation in line with your risk tolerance.

Its primary goal is not to boost long-term gains. Rebalancing is a risk management strategy and hence it is crucial to comprehend the significance of the term “Risk” in investing.

Risk is the biggest component that affects investment decisions and the all-around portfolio returns.

In simple words, the risk is the possibility of something bad happening that can result in an undesirable consequence. The economic realm is exposed to many variations of financial risks. Risks are classified under several categories. This depends on the positioning of your investment on the broader financial spectrum.

Some examples are:

☑ Asset-backed risk

☑ Credit risk

☑ Foreign investment risk

☑ Currency risk

☑ Liquidity Risk

☑ Stock Market Risk, and

☑ Interest Rate Risk.

The investing philosophy roughly divides risk into two types — Systematic risk and Unsystematic risk—in the interest of simplification and greater alignment with the subject.

Understanding Systematic Risk

In finance, systematic risk is vulnerability to events that affect aggregate outcomes.

Sounds mouthful? let us make this snackable!

Systematic risk is a risk within the entire system. This is the kind of risk that applies to an entire market or market segment. All investments are affected by this risk.

For instance, there is a risk of a government failing, inflation, a credit crisis or collapse, a war, natural calamities like earthquakes, or being struck by a meteorite that once wiped out the dinosaurs.

It is almost impossible to protect a portfolio against this risk. It can’t be entirely diversified away and hence it is also known as un-diversifiable risk or market risk. Unless you hold the power to directly negotiate with governments, influence earthquakes, or be able to travel through intergalactic civilizations it’s a risk that you live with at all times.

Understanding Unsystematic Risk

Unsystematic risk is also known as residual risk, specific risk, or diversifiable risk. It is unique to a company or a particular industry.

For example, union strikes, lawsuits, and such events that are specific to a company, and can to an extent be diversified away by other investments in your portfolio are unsystematic risks. Unsystematic risk is controllable and can be diversified through layering or stratification.

Layering in an equity portfolio is often achieved by investing in (a) various stocks of (b) several handpicked companies (c) across different related and (d) unrelated sectors. This type of risk can be further curtailed by diversifying across uncorrelated assets such as (e) gold, (f) debt, (g) commodities, or (h) real estate.

Multi-asset portfolios are always difficult to manage and hence there is a detailed field of academics that works purely in core diversification strategies across all the instruments highlighted above.

The Subtle Art Of Not Rebalancing

Portfolio rebalancing is the process of buying and selling assets to align your portfolio with the target asset-allocation percentages you determined in your “investment plan“. Over time, a portfolio can become unbalanced, or different from your target asset allocations.

This may happen due to changes in asset and asset class performance, changes in your objectives or risk-tolerance level, and the infusion of new capital or new asset classes that you consider desirable.

Just like we prune the plants in a garden to ensure controlled and healthy growth, the act of rebalancing aims to trim the overgrowths; thereby minimizing unsystematic portfolio risks. The shaved-off capital is constantly reinvested to equalize other holdings.

Key Rebalancing Strategies

Several rebalancing strategies have been extensively covered in our comprehensive course. In this post, however, we will examine two primary rebalancing techniques-

💬 Periodic-based rebalancing &

💬 Percent-based rebalancing

Periodic-Based Portfolio Rebalancing

You must decide on the “periodic-based rebalancing” frequency, which may be monthly, quarterly, or yearly. After each designated period, you will rebalance your portfolio to make it consistent with the target asset allocation percentages listed in your investment plan.

The advantage of periodic-based rebalancing is that it is a simple method. The disadvantage is that it does not account for current market performance, which influences overall portfolio performance.

By making practical decisions based on the current bull, sideways, or bear markets, this strategy can be further improved.

Percentage Range Portfolio Rebalancing

In percent range rebalancing, you rebalance your portfolio’s target asset-allocation percentages that drift from a predetermined percentage to your target proportions. For example, imagine you find this glorious stock and decide to invest 10 percent of your portfolio totals into it.

After a year or so, you observe that your stock has had a strong bull run that has increased its value which is now worth 15 percent of your total portfolio. You simply shave off that 5 percent excess by selling some stocks, bringing your total exposure back to 10 percent.

In a similar scenario if, due to some reason your glorious stock sheds its value by 5 percent owing to the volatility, you buy more of it at a lower cost thus re-claiming your 10 percent exposure. The advantage of this method is that it is easy to implement because asset performance will indicate when you should rebalance.

The drawbacks include the difficulty in determining the optimal range. This suggests that assets with higher goal percentages and greater volatility require more frequent rebalancing than those with lower target percentages and greater stability.

Important Rebalancing Considerations

✓ Transaction Costs

Every time you buy or sell equity it attracts transaction costs. A high buying and selling frequency can devour substantial profits over time.

✓ Taxes

You can’t avoid the tax implications arising from the churn. The more you stir your assets, the more you will pay in taxes. This is one of the key reasons why most actively managed funds fail to outperform their benchmarks, especially after transaction costs and taxes have been accounted

for.

✓ Market Risks

Markets are in constant momentum. The minute you sell an asset and till the time you buy the next one, you are exposed to market risk. Your plan to buy the next potential stock can go bust if that stock substantially rises in value by the time you reach for it.

Uncertainty and confusion must be avoided during buy-sell swaps to maintain momentum.

Conclusion

The strategy that feels most convenient will probably come out on top when discussing the best rebalancing technique. To avoid trouble, you can constantly keep balancing your portfolio by infusing “new money” in tandem with your ongoing exposures. You can use this as a counter technique to restore your asset mix. This one especially works well for young investors with longer investment horizons.

Our definition of a young investor refers to those individuals who are aggressively accumulating great stocks at the moment for long-term goals such as retirement.

For smaller portfolios (less than ₹1 crore), a combination of periodic-based rebalancing and per-cent-range rebalancing typically works effectively. These strategies can also be combined with the “new money” infusions derived from dividends to reduce frequent portfolio churn. For greater efficiency, any losses acquired during the rebalancing process must be written off as short-term capital losses (STCL).

You can read more about STCL in our focused top-10 article. Alternatively, if you are not a DIY-type investor, you may very well outsource this undertaking by means of employing a PMS scheme or through a registered financial advisor for a fee. Portfolio rebalancing smooths the profitability of your stock investments, forcing you to buy low and sell high.

Rebalancing techniques may appear to be a bit difficult and time-consuming, but they are essential to effective investing.

Did you find the information documented in this article helpful?

🔔 Investing is expensive, but leaving comments on this blog is free!