Secure your future effortlessly with the National Pension Scheme (NPS), the ideal way to build your retirement fund. Dive into our expert guide and kickstart your NPS investment journey today.

The Context

The question isn’t at what age I want to retire, it’s at what income — George Foreman

What makes India a diverse country?

💬 Rich culture, breathtaking landscapes, and our pension systems!

Except for private players, the US has two main pension systems: Social Security and the Public Employees Retirement System.

The United Kingdom also contends nicely with two primary pension systems known as the Statutory State Pension system and an Earnings-Related additional pension known as the State Second Pension. India, however, takes first place thanks to its several, extremely complex pension systems that are tailored for different market groups.

Here is just a small sample of our diverse pension systems:

☑ Scheme for Government Servants — This includes the State Government Pension scheme; Central Government Pension Scheme and NPS for newly joined employees

☑ Scheme for Public Sector Employees — This entails a Public Sector Pension policy and NPS for newly joined employees

☑ Scheme for Private Sector Employees — This includes EPFO, EPF, EPS; Occupational Pension; NPS, and Mutual Funds

☑ Voluntary Schemes — PPF; NPS; Pension Plans by life insurance companies and Mutual Fund Schemes

☑ National Social Assistance Programme (NSAP) for the elderly and poor

☑ Pradhan Mantri Shram Yogi Maan-Dhan (PMSYM) for poor laborers in the unorganized sectors

☑ Atal Pension Yojna (based on the NPS framework)

What’s The Big Deal?

The complexity of so many systems nevertheless is a blessing in disguise when it comes to the predicament we are in – There’s just too much diversification to handle at once! As per the World Bank labor force data; India has about 470 million people engaged in employment across numerous sectors.

According to another contrasting report by the World Economic Forum on Global Human Capital – Only 7.4 percent of the working-age population in India is covered under a pension program. That compares with 65 percent for Germany and 31 percent for Brazil.

The presence of so many schemes had initially almost achieved the focus on an inclusive pension system. However, still, a large proportion of India’s population remained under-represented in the pension schemes and there seemed to be considerable room for proliferation in this sector.

India is a growing economy with a sharp future ahead of us.

So, as an act of standardization; in 2004, the National Pension System Trust was rolled out by the Indian government and became the only universal scheme to handle the assets and funds of all subscribers.

The NPS started with the decision of the Government of India to stop defined benefit pensions for all its employees who joined after 1 January 2004. It is a government-sponsored pension and Investment scheme launched as a sustainable solution to help secure the financial life of an individual after retirement.

The NPS system was initially launched for government employees. However, after much deliberation in 2009, it was opened to all sections including private employees. After the Central Government, various State Governments adopted this architecture and implemented the NPS. All government employees who have joined on or after the date of NPS introduction are mandatorily covered as per the government guidelines.

The scheme now allows subscribers to contribute regularly to a pension account during their working life. R.I.P. the good old days of defined benefit pensions where an employer used to promise a specified pension payment, a lump-sum combination thereof on retirement.

For the record, rather than relying solely on individual investment results, a defined benefit system (DB) is used to determine an employee’s benefits based on their history of earnings, length of service, and age.

How Does It Work?

Simply put, NPS can be compared to a low-cost, closed-ended mutual fund with a predetermined exposure to equities and equity shares. Because of this, investment money is better protected. The individual savings are pooled into a pension fund which is managed by Pension Fund Regulatory and Development Authority (PFRDA) regulated professional fund managers.

The approved investment guidelines help pool your money into diversified portfolios comprising Government Bonds, Bills, Corporate Debentures, and Shares. These contributions are assumed to grow and accumulate over the years, depending on the returns earned on the investment made. It is governed by the statutes where the expense ratio or fees for managing the funds is capped.

NPS is conceivably the lowest-cost investment- pension scheme. In most cases, the total recurring expenses inclusive of the fund management fee and all other handling and administrative charges can work out to be only around 0.21% per annum.

Types Of NPS Accounts

Tier I accounts (primary) and Tier II accounts (voluntary) are the two primary categories of NPS accounts.

Tier I NPS Account

This is the most basic type of NPS account that is opened for eligible employees working in the government or private sectors. When you open a Tier I NPS account, you get a unique 12-digit identification key known as Permanent Retirement Account Number (PRAN). The minimum contribution that you need to make while opening a Tier I account is ₹500. To keep the account active, you need to contribute a minimum of ₹1,000 annually.

While there’s no cap on the maximum investment in this account, the money that you invest gets locked until you turn 60. Once you attain the age of 60, you can only withdraw 60% of the accumulated corpus.

The rest 40% corpus is used to buy an annuity plan from a PFRDA impaneled Life Insurance Company that will pay you a monthly pension depending on the leftover accumulation. An annuity is a fixed amount of money that you will get each year for the rest of your life. Your investment towards a Tier I account qualifies for tax exemption under section 80CCD of the Income Tax Act 1961.

Tier II NPS Account

Tier II NPS account is an add-on account that provides you with the flexibility to DIY (invest and withdraw) from various schemes available under NPS without any exit load.

Tier II NPS account can only be opened if you have a Tier I account under your name.

You can open this account with a minimum deposit of ₹1,000 and post that you can invest as much as you want.

Tier-II accounts however don’t enjoy any tax exemption or benefits.

Asset Allocation Choices

The sophisticated choices and asset allocation mechanism of NPS are what give it its charm. For those who are not financially savvy, this also serves as a self-regulating financial advisor. Every investor gets 4 diversified options to choose from namely – Equities, Government Securities, Corporate Debt & Alternative Investments.

These options are further bundled as Active asset allocation (where you manage your risk) and Auto asset allocation (where they manage risk for you).

Active Asset Allocation

It’s a good and flexible option if you’re a DIY type of investor. When you choose Active asset allocation, you influence the inflow of money among each asset class. The capping is however limited to 75% towards equity, also Once you cross the age of 50, the equity exposure would come down to protect you from stock market volatility risks.

Auto Choice Asset Allocation

This is a pre-bundled option; much like an auto advisor. Here, you further get three options to pick from with some capping constraints under

💬 Aggressive Lifecycle Funds — 75% Equity exposure capped till 35 years of age

💬 Moderate Lifecycle Fund — 50% equity exposure capped till 35 years of age

💬 Conservative Lifecycle Fund — 25% equity exposure capped till 35 years of age

Depending on your risk appetite, you can opt for any of these options and focus on your day-to-day life as the magic of compounding unfolds on your pension account.

How To Get Enrolled?

Online NPS Enrollment

To open an NPS account all you need is a set of 6 essential things:

- Adhaar Card

- Netbanking Access

- Copy of Cancelled Cheque

- Passport Size Photos

- Scanned Image of your signatures and

- PAN Card.

Once you are ready with these documents and a hot cup of coffee, follow these 10 simple steps –

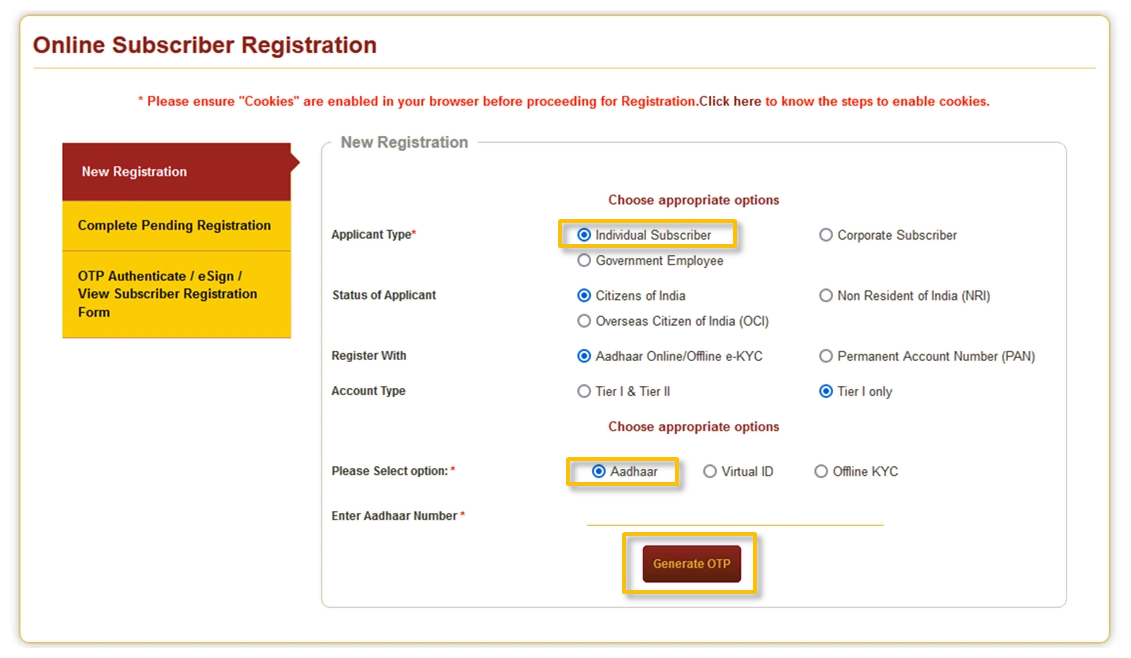

🖱 Step 1- Visit the official NPS website and click on the ‘National Pension System” selection in the top right-hand corner.

🖱 Step 2- Select ‘Individual’ and feed in your Adhaar Card and Pan Card number

🖱 Step 3- You will now receive a one-time password (OTP) on your registered mobile number

🖱 Step 4- Enter the OTP and click on ‘Continue’, this will generate an acknowledgment number that will have your name, select ‘OK’

🖱 Step 5- Enter your details and click on ‘Save and Proceed’

🖱 Step 6- In this step, you select your asset allocation as ‘Active’ or ‘Auto’.

🖱 Step 7- Remember to fill in the Nomination details

🖱 Step 8- Upload a copy of the canceled cheque of your bank account along with those scanned signatures if yours

🖱 Step 9- You will be asked to pay a minimum of ₹500 as your account opening deposit

🖱 Step 10- Use net banking to transfer the funds and you will automatically receive your PRAN number and the payment receipt.

Offline NPS Enrollment

To open an NPS account offline, you will need to visit any point of presence (POP) appointed by the PFRDA. For your comfort, most banks are now already enrolled as POP.

Visit the POP with original KYC documents for verification along with photocopies for submission. Fill up the prescribed forms as per the directions to get your 17-digit receipt number. Upon verification, you will receive your NPS kit at your registered address along with the PRAN number.

You will also receive an SMS on your registered mobile number about the process notifications. It’s a seamless process in most cases.

Conclusion

To take care of your post-retirement days and live a stress-free existence, you must have financial security after retirement. Many people tend to forget about safeguarding their financial future due to a variety of distractions, misdirections, and haphazard decisions. To start, NPS can be a simple answer to this issue. But, due to a lack of awareness, NPS appears to be a little under-penetrated in our economic system.

As per a recent stat published on Statista by Sandhya Keelery; The National Pension System had only about 14 million subscribers (against 470 million working population) as per the financial year 2021 across India.

NPS might not seem like the ideal tool in the toolbox for inquisitive, astute, and financially educated Investors who prefer to hang out in investing forums like this one. However, due to its low-cost setup and clever safety features, it does have some special advantages.

Feel free to leave your opinions or your preferred pension system in the comments section.

🔔 Investing is expensive, but leaving comments on this blog is free!

5 Comments

NPS is a great option for many individuals, but the lack of custody of over 40% of the capital after retirement could be a limitation for educated people.

To your point, how many Indians are educated? The literacy rate and financial literacy rate are absolutely two seperate things!

About 25% Indians are financially literate. It’s not a degree, it’s a lifelong process.

Annuity attracts tax. Not a good investment. Disciplined investors should be better off with Stocks and Fixed deposit.

Guaranteed pension demands sacrifices 😂