Is the conventional banking system facing a transformative wave led by Neo-banks? Dive into this article as we explore the trailblazers shaping the landscape of modern finance.

The Context

Neo-banks are upending the traditional banking industry by using technology and artificial intelligence (AI) to provide customers with a choice of individualized services. Neo banks, like discount brokers.

They are a sort of direct bank that only does business online and does not use conventional physical brick-and-mortar networks.

In our country, they primarily offer their services through digital applications and connected portals, capitalizing on the rise of the internet, the acceptance of technology, and the love of smartphones. These banks are also referred to as online banks, internet-only banks, virtual banks, or digital banks.

Globally there are 2 types of neo-bank formats — A full-stack neo-bank and a front-end focused neo-bank.

A full-stack neo-bank is a standalone bank with a banking license and can operate completely independently. Comparatively, a front-end-focused neo-bank does not have its banking license and must operate in partnership with either a traditional or legacy bank to provide its services to customers.

Since full-stack neo-banks are still not permitted in India by the Reserve Bank of India (RBI), all neo-banks in our country operate through partnerships with conventional banks. Customers’ money is thus kept in an underlying real-bank account.

With the involvement of an essential banking body, the RBI’s insurance guarantee of up to ₹5 lakhs under Deposit Insurance and Credit Guarantee Corporation (DICGC) extends to neo-banks as well. They are subject to fewer laws and little credit risk, which is advantageous to users. Neo-banks can keep their costs low as a result.

Neo-products are generally inexpensive, with no monthly maintenance fees. Variations of these products include savings accounts, prepaid cards, bill payments, and money transfers. These banks distinguish themselves from their more established rivals by applying innovative problem-solving techniques to a specific branch of banking.

Purely digital characteristic helps with efficient change turnarounds that help mobilize and tailor their products and services. This compartmentalized approach makes banking simpler, faster, and more convenient for the end consumers.

Neo-banks are now captivating their customers with features like easy spend analytics, high interest rates, and personalized rewards for both consumers and merchants. In our opinion, neo-banks are far from disrupting the traditional banking system as yet because they are currently attracting low-value clientele. They do however have the reasonable potential to devour a big chunk of the banking pie in the long run.

According to Grand View Research (Report ID: GVR-4-68039-324-2), the global neo-banking market size was valued at over $47 billion in 2021 and is expected to grow at a compound annual growth rate (CAGR) of over 53% from 2022 to 2030.

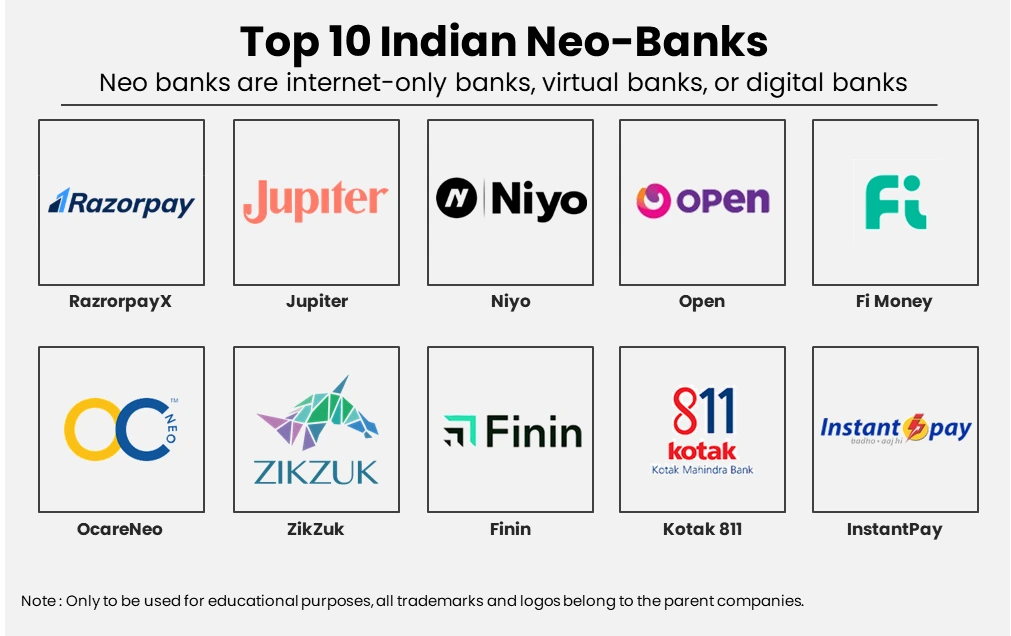

The rising demand for convenience among customers in the banking sector is expected to drive market growth in this segment. Here is our ranking of the top ten neo-banks currently operating in India. These institutions can help you simply manage your out-of-pocket personal money, even though they might not help you reach your financial goals.

1. RazrorpayX

RazorPayX is a powerful and modest business banking alternative founded by Harshil Mathur, Founder, and CEO, in 2014. With a completely digital account, automatic payments, payables, corporate cards, and deep financial insights all in one place, RazorPay X is built to supercharge the banking and finance of Indian companies.

Intending to automate laborious, repetitive financial chores and offer in-depth insights into cash flow, this fintech solution primarily targets business owners and online retailers. They offer credit solutions, streamline payouts, and support current account ledgers.

2. Jupiter

Jupiter is a bank that is built to serve the digital customers of today with a banking service that keeps pace with them. Founded by fintech veteran Jitendra Gupta, with Jupiter the users can create bank accounts in a flash.

Additionally, consumers have the option of automating their savings in pots. They can also receive current information and a thorough breakdown of their spending. Jupiter claims to have zero balance account facilities and extends instant support to its users.

Additionally, it aids customers in earning incentives on every transaction, which are equal to 1% of the value of their debit card and UPI purchases.

3. Niyo

Founded in 2015 by the banking industry and payments expert Vinay Bagri Virender Bisht, Niyo boasts of “Making Banking Smarter, Safer and Simpler”. Niyo brings a suite of useful banking products-

🪙 Niyo X- An efficient app that offers customers the facilities of savings and helps them manage wealth without hassles.

🪙 Niyo Money- Empowered by Robo-advisory, Niyo Money helps customers grow and manage wealth.

🪙 Niyo Global- With Niyo Global the customers need not worry about round-the-clock support along with earning up to 5% interest against their savings.

🪙 Niyo Bharat- Marketed as an open banking platform Niyo Bharat is an app that ensures salary cards for employees.

4. Open

Open is a well-recognized digital business banking solution that is trusted by 20,00,000+ Indian businesses. Headquartered in Bengaluru, Open aims to simplify business banking.

Founded in 2017, the Open Business Accounts offer VISA co-brand business cards that help in banking, payments management, accounting, and more. The company acquired another new banking startup Finin on December 14, 2021, for $10 million

5. Fi Money

With the tagline “Banking Just Got Smarter”, Fi Money is designed as a new bank with secure digital banking services for the working professionals of today. Founded by the co-founders of GPay, Sujith Narayanan and Sumit Gwalani Fi offers a smart zero-balance savings account for customers in a way that they can manage their money better.

Along with easy savings options that help the users get interested by up to 5.1%, Fi Money also brings them an assistant that can solve almost any of the user queries. Additional advantages that customers can take advantage of with the aid of Fi Money include interesting rewards and safe financial services.

6. OcareNeo

There’s a lot unique about this one. Driven by the tagline “Your Digital Health Passport”, Dr. Neeraj Sheth founded OCareNeo to help this generation focus on their medical needs.

OCareNeo helps its customers dive into their digital health journey with which they can get instant access to their health and that of their families along with financial information.

The company offers a unique facility of a Digital QR code that keeps the owner’s health history and insurance details, along with a Digital Card and Digital Piggy Bank to pay for medical expenses and save for health. Additionally, OCareNeo provides consumers with a list of safe and simple insurance coverage to assist them in protecting their health.

7. ZikZuk

ZikZuk is an Indian SME neo-banking startup founded in 2020 by Raj N that is built to foster the growth of Indian SMEs. Among its products and services, ZikZuk offers FoundersCard, a credit card that empowers business entrepreneurs with the best credit scores by bringing numerous exciting rewards.

Furthermore, ZikZuk also helps the company founders get unsecured credit to satisfy their immediate capital requirements. Entrepreneurs can manage their company finances easily with the help of ZikZuk. Another feature that ZikZuk provides is connected banking.

8. Finin

Finin is an uber neo-banking startup founded in 2019 that strives to bring “a new approach to banking.” The first-ever consumer-facing Neo-bank offers easy account opening and management facilities via a comprehensive app.

Modern artificial intelligence technology powers this system. Finin provides consumers with smart advice to help them make better financial decisions. The company has now been acquired by Open (on December 14, 2021), and will result in adding value to Open and its band of SMEs.

9. Kotak 811

811 by Kotak or Kotak811 is a new bank-based banking concept that offers personal accounts with debit cards for individuals. Opened after November 8, 2016, the day of demonetization, which changed everything.

Kotak Mahindra came up with this new concept of easy, online banking services for its customers via Kotak811, where the numbers reflect the date of demonetization. Indian citizens can rapidly open paperless, paperless, simple-to-use, and simple-to-handle mobile bank accounts with the aid of Kotak811.

10. InstantPay

Billed as India’s largest new banking platform, InstantPay claims to offer full-stack digital banking services for businesses and individuals but still mentions ICICI, Axis, Yes Bank, and IndusInd Bank as their banking partners.

As per our research, On 24th November 2021, government think-tank CEO Amitabh Kant of Niti Aayog proposed setting up full-stack digital banks and that’s yet to happen.

Empowered by the slogan, “Banking for the New India”, InstantPay extends easy banking options via which the users can spend, save and manage money online. Shailendra Agarwal established InstantPay in 2012 to improve the client experience when banking.

This completes our list of the Top 10 neo-banks.

Conclusion

The banking industry is fiercely competitive. The advancement of this list is based on evaluating ongoing expansion, customer demands, and the winds of change rather than any particular biased priority.

Therefore, this selection shouldn’t be interpreted as a way to choose the best. Due to their expense and reliance on outdated technology, consumers are becoming increasingly frustrated with legacy banking service providers. The transition to digital-only banking has been sped up by these drawbacks together with a greater desire for digital solutions.

Money deposited in a neo-banking account is as secure as it would be in an Indian ordinary bank account, even though Neo-bank’s security can occasionally rely heavily on outside security firms. This is mainly due to their front-end format.

If you think we’ve overlooked a Neo-fintech that you think should be featured here, feel free to remark!

🔔 Investing is expensive, but leaving comments on this blog is free!

1 Comment

Brilliant post.