The Rise Of The “Dumb Money”

India’s investor IQ crisis is unfolding in real time. The financial markets are witnessing unprecedented retail participation, with over 14 crore demat accounts opened as of 2024. Yet beneath this seemingly positive narrative lies a disturbing truth, a growing financial literacy crisis in India. We are witnessing the systematic dumbing down of an entire generation of investors.

This is not mere market volatility or cyclical losses; it’s the creation of a cognitively impaired investment ecosystem that threatens to undermine decades of financial progress.

The Cognitive Collapse Of Attention Spans

The foundation of intelligent investing has always been the ability to analyze, deliberate, and make informed decisions. However, recent studies reveal a catastrophic decline in cognitive abilities that directly impacts investment decision-making.

Microsoft’s landmark research shows that human attention spans have plummeted from 12 seconds in 2000 to just 8 seconds in 2025.

This is now shorter than that of a goldfish, creating what researchers term “cognitive overload”. The implications for investment decisions are profound, how can aspiring investors conduct proper due diligence when they cannot focus on a single task for more than eight seconds? This growing distraction and lack of analytical discipline sit at the heart of the financial literacy crisis in India, where surface-level understanding now replaces deep financial reasoning.

The Flynn Effect, which documented rising IQ scores throughout the 20th century, has dramatically reversed. Studies across Scandinavia, Britain, Germany, France, and Australia show declining IQ scores since the turn of the 21st century.

In India, this cognitive decline manifests most visibly in investment behavior, where 91% of retail F&O traders consistently lose money, representing not market inefficiency but cognitive failure.

The Death Of Sensible Reading

One of the most alarming indicators of intellectual decline is the collapse of reading habits. Only 34.6% of children aged 8-18 now enjoy reading in their free time, the lowest level in nearly two decades. In India specifically, 90% of printed books fail to exceed sales of 2,000 copies unless they carry explicit titles like S*it or F*uk.

This shift from deep reading to superficial scrolling has rewired our brains for instant gratification rather than analytical thinking a major driver behind the financial literacy crisis in India that leaves investors unprepared for complex financial decisions. The National Endowment for the Arts found that less than 38% of Americans read a novel or short story in 2022, down from 45% in 2012.

In India, the situation is even more dire, with libraries closing and reading becoming increasingly unpopular among youth.

The consequences for investment decisions are immediate and devastating. Complex financial instruments like derivatives or Deep Value assessments require sustained attention and analytical thinking. Precisely the cognitive skills being eroded by our digital-first culture.

Social Media Is The New Financial Advisor

Perhaps the most dangerous development is the rise of “finfluencers”or financial influencers who have replaced traditional advisors in the minds of retail investors.

SEBI’s 2025 survey reveals that 62% of retail investors make investment decisions based on social media influencer recommendations. Even more concerning, 93% of their audience rates these influencers as moderately to highly trustworthy.

This represents a fundamental shift from evidence-based investing to entertainment-driven decision-making. Social media platforms, designed for engagement rather than education, promote content that generates views rather than wealth.

The average engagement with influencer-generated posts is 8 times higher than branded financial content, creating an environment where entertainment value trumps educational merit.

The psychological mechanism at work is FOMO (Fear of Missing Out), which now drives investment decisions more than fundamental analysis. Social media creates an illusion of easy profits through cherry-picked success stories while hiding the systematic losses experienced by the majority.

The Entertainment-ization Of Everything

What was once a separate professional class “entertainers” has now infiltrated every aspect of life, including financial education. The proliferation of short-form content on platforms like Instagram Reels and YouTube Shorts has transformed serious financial education into bite-sized entertainment.

India’s influencer marketing industry is projected to reach ₹3,375 crore by 2026, growing at 18% CAGR. This growth comes at the expense of traditional, qualified financial advisory services. The result is a generation that seeks financial guidance from entertainers rather than experts, leading to entertainment-based rather than evidence-based investment decisions.

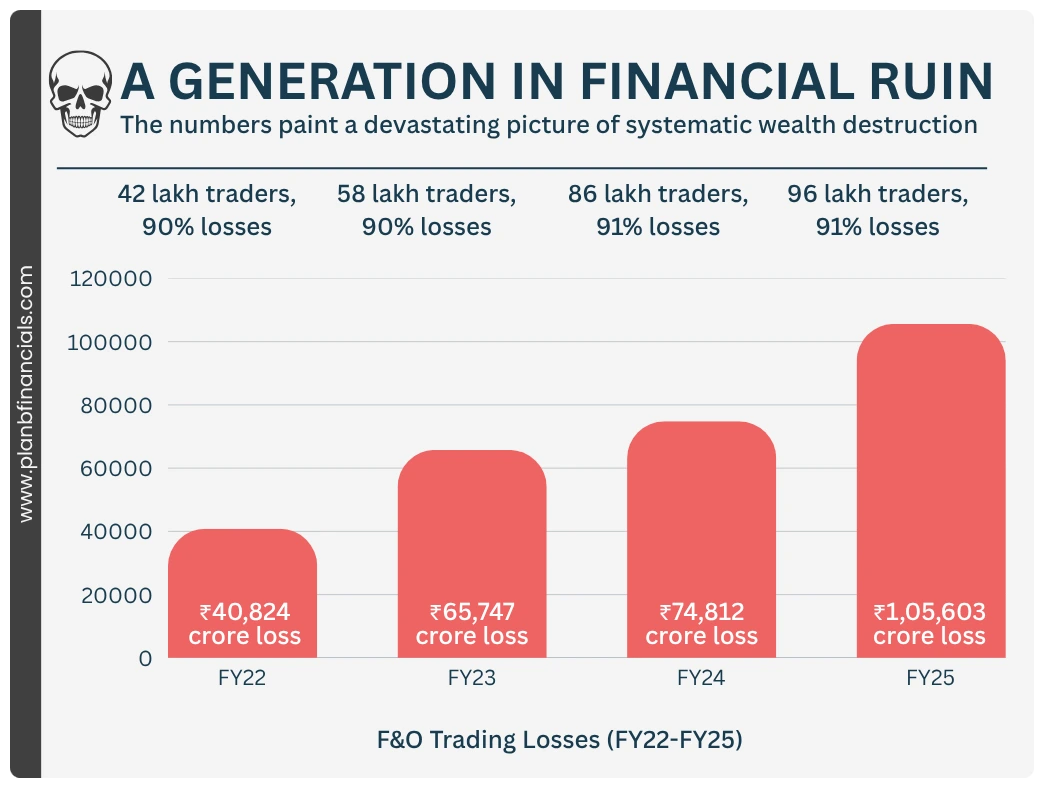

The consequences are evident in trading behavior. Retail investors lost ₹2.87 lakh crore in F&O trading between FY22-FY25, with losses accelerating each year despite (or perhaps because of) increased social media influence.

AI, Algorithms, And The Death Of Critical Thought

Artificial Intelligence, while revolutionary, is creating a new form of cognitive laziness.

Recent studies show that increased AI usage correlates negatively with critical thinking skills. Younger individuals (ages 17-25) exhibit the highest AI dependence and lowest critical thinking scores. The phenomenon of “cognitive offloading” or relying on AI to reduce mental effort is creating investors who cannot independently analyze financial information.

When AI tools provide instant answers, users lose the cognitive struggle essential for developing analytical skills. This creates a dangerous cycle where investors become increasingly dependent on external tools while their independent reasoning abilities atrophy.

A Generation In Financial Ruin

This represents a 160% increase in losses over four years, with consistently 90-91% of traders losing money. The average loss per trader has jumped from ₹74,812 in FY24 to ₹1.05 lakh in FY25.

These are not market corrections or temporary setbacks, they represent systematic cognitive failure at scale.

The IQ-Decision Maker Paradox

Perhaps most alarming is the emergence of what can be termed the “IQ-Decision Maker Paradox”, as overall cognitive abilities decline, individuals with lower analytical skills are increasingly making critical financial decisions.

The democratization of investing through technology, while positive in principle, has removed traditional gatekeepers who once prevented cognitively unprepared individuals from accessing complex financial instruments.

Financial literacy in India stands at just 27% compared to 52% in advanced economies. Yet these same individuals are trading complex derivatives and making investment decisions that would challenge even sophisticated investors.

Financial Literacy Is the New National Emergency

The Path Forward For Cognitive Rehabilitation

Solving this issue begins with recognizing that it’s not just a financial problem; it’s a cognitive crisis that demands action on multiple fronts.

Education needs a fundamental reset. Financial literacy should be treated as a core life skill that builds focus and analytical thinking, not as bite-sized entertainment.

Regulators too have a critical role. SEBI’s recent steps to restrict easy access to F&O trading are a start, but far from enough. Stronger interventions are needed to safeguard investors who are increasingly vulnerable to cognitive and behavioral traps. At the individual level, a digital detox is essential. Investors must consciously limit their social media exposure and re-engage with traditional, deeper forms of financial learning that strengthen long-term thinking.

Finally, investment education itself needs an upgrade. Courses and programs must include training that actively rebuilds attention spans and sharpens critical reasoning.

The rise of “dumb money” isn’t accidental, it’s the logical outcome of a culture that rewards entertainment over understanding and instant gratification over patience. Without urgent action, India risks not only widespread financial losses but also a slow intellectual decay of its investor base.

The path forward is clear, either confront this cognitive crisis with decisive reforms and awareness, or continue watching an entire generation sabotage its financial future through mental complacency.

🕒 The data suggests we are running out of time to choose wisely.