Enter a world of financial security with fixed-income investments – something important to have in your investment toolbox. In this blog post, we’ll reveal ten choices, like bonds and CDs, that can help you lock in a steady income you can rely on.

The Context

To have a Full Stomach and Fixed Income are no small things — Elbert Hubbard

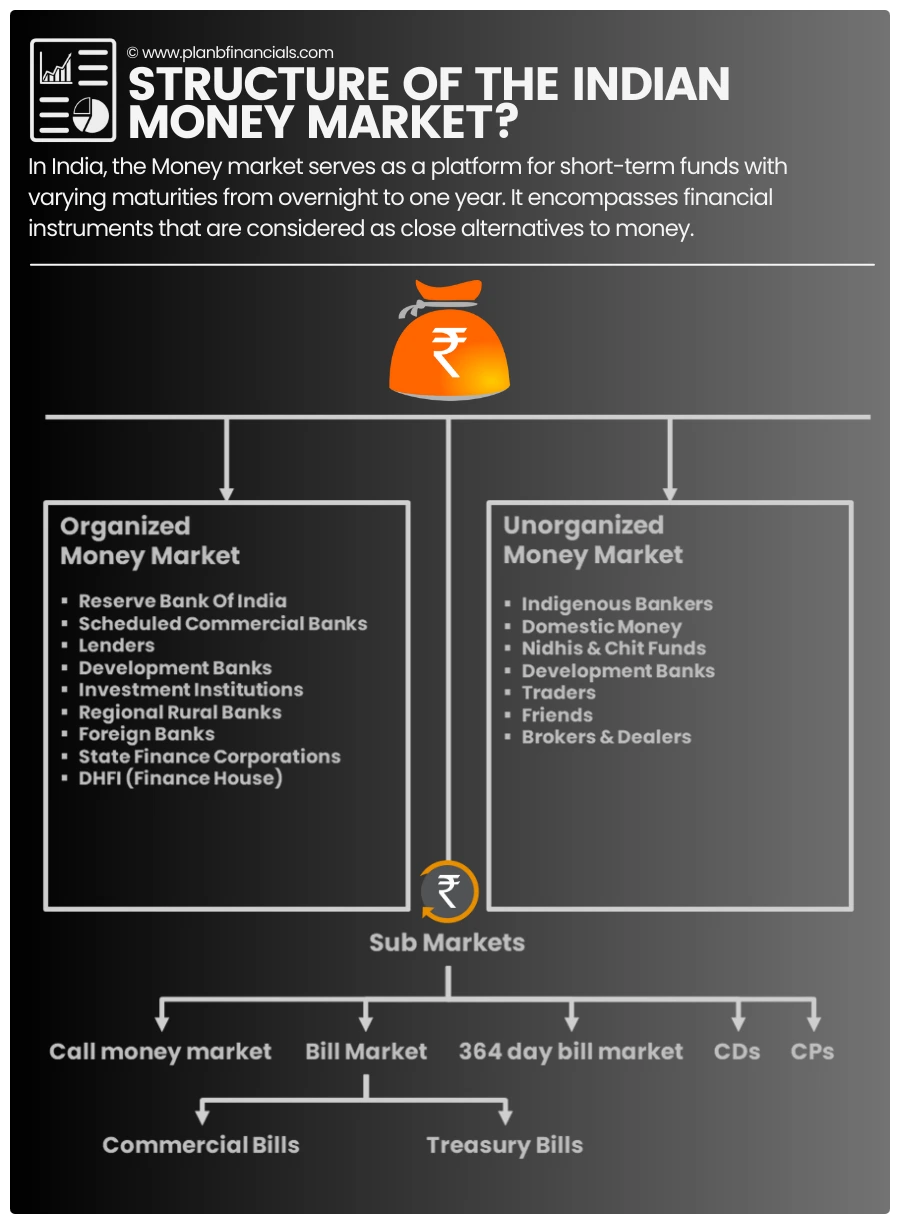

The great Indian debt market is a territory where investment loans are bought and sold in many forms.

Fixed-income markets chiefly constitute Money and Bond markets. The fundamental difference between the money market and the bond market is that the money market specializes in very short-term debt securities.

These are the debts that mature in less than one year.

One of the biggest debt markets in Asia is India. Several variables, such as new instruments, more liquidity, the deregulation of interest rates, and enhanced settlement systems, have helped it flourish quickly. Banks, Financial Institutions, Insurance Companies, Foreign Institutional Investors FIIs, and Mutual Funds are the main players in the Indian debt markets.

Debt instruments available in the market can be broadly categorized as those issued by Corporations, Banks, and Financial institutions and those issued by State and Central Governments. Before diving into the world of Debt and related instruments, it’s imperative to understand that Debt is not one hundred percent risk-free.

The common risks associated with any debt investments are —

☑ Interest rate risks

☑ Inflation risks

☑ Credit risks

☑ Liquidity risks and

☑ Reinvestment risks

While Corporate papers carry credit risk due to changing business conditions, most Government securities are perceived to have zero credit risk. Interest rate risk is one of the only hazards that are present in all debt securities and this is highly dependent on a variety of macroeconomic factors.

The largest segment of the Indian debt market consists of Government Of India securities where the daily trading volume is more than ₹10,000 crore. Instrument tenors range from short-dated treasury bills to long-dated securities extending up to 30 years.

Investors with a lower risk tolerance favor debt products. Additionally, they are employed to achieve various diversification strategies. The money market in India is regulated by both the Reserve Bank of India and the Securities & Exchange Board of India (SEBI).

The fixed income market is perceived as more complicated than equity (stock) markets.

The “Top 10 Fixed Income Securities” that every DIY investor needs to be aware of are listed below.

1. Call Money

The Call Money market is an important segment of the Indian money market. Under the call money market, funds are transacted on an overnight basis This means, that lending and borrowing from the call money market are usually for just 1 day.

As per the RBI guideline, the participants in the call/notice money market currently include:

≡ Scheduled Commercial Banks (excluding Regional Rural Banks)

≡ Development of Financial Institutions

≡ Cooperative banks (other than Land Development Banks), and

≡ Primary Dealers (PDs),

both as borrowers and lenders.

2. Notice Money

The Notice Money market is another component of the Indian money market where the funds are transacted (lending and borrowing ) for a period between 2 days and 14 days. Similar to Call money, participants in the notice money market currently include banks, Primary Dealers (PDs), Development Finance Institutions, Insurance companies, and select Mutual Funds.

Banks and PDs can operate both as borrowers and lenders in the market. Non-bank institutions, which have been given specific permission to operate in the call/notice money market can operate as lenders only.

3. Term Money

Corresponding to Call and Notice money, the “Term Money” market is the third sub-extension of the Indian money market. When there is borrowing and lending of funds for a tenor of more than 14 days, it simply refers to “Term-Money”

4. Treasury Bills

Treasury Bills or T-bills are short-term debt instruments issued by the Government of India. The funds raised through T-Bills are generally used to meet the short-term requirements of the governments.

These types of instruments usually aid them in reducing the overall fiscal deficits of the country. Treasury bills (T-bills) offer short-term investment opportunities, normally up to one year. They are thus useful in managing short-term liquidity. At present, the Government of India issues four types of treasury bills, namely, 14-day, 91-day, 182-day, and 364-day.

Treasury bills are zero-coupon securities and pay no interest. In debt markets, zero-coupon security is a security that pays no interest and trades at a discount to its face value. For Example, an 182-day treasury bill with a face value of ₹180 can be purchased at a discount of ₹172.44.

Upon maturity, the investor receives the entire nominal value of ₹180 to realize a profit of ₹7.56. T-bills are sold through auctions and as per an RBI publication “A 14-day and 91-day T-bills are auctioned every week on Fridays, 182-day and 364-day T-bills are auctioned every alternate week on Wednesdays.”

The Reserve Bank of India issues a calendar of T-bill auctions. It also announces the exact dates of the auction, the amount to be auctioned, and payment dates by issuing press releases before every auction. Retail investors can also invest directly in T-Bills by opening an online Retail Direct Gilt Account (RDG Account) with the Reserve Bank of India (RBI). These accounts offer the convenience of directly linking savings bank accounts to participate in the issuance of government securities and secondary market operations.

5. Commercial Bills

A Commercial Bill is an instrument that helps companies get advance payment for the invoices they raise after making sales to their customers. Please note that Commercial bills are different from Commercial papers.

Commercial papers (next on the list) are used by banks to meet their short-term obligations while a Commercial bill is an instrument that helps companies to get advance payment for the invoices they raise after making sales to their customers. The commercial bill market is an important source of short-term funds for trade and industry as it helps provide liquidity and stimulate the money market.

In India, all commercial banks play a significant role in this market.

6. Commercial Papers

Commercial Papers are short-term unsecured money market instruments. An unsecured instrument is a debt instrument that is not secured (backed by any collateral). They are used as a means to obtain a loan, acting as a protection against potential loss for the lender should the borrower default on his payments.

Abbreviated as CP, these instruments are issued as promissory notes by big corporations that possess a good credit rating.

There is no collateral support for CPs hence only large firms with considerable financial strength can issue this instrument. Credit rating is the key to investing in Commercial papers. Retail investors can subscribe to CPs either in physical form or in dematerialized form, but you’ll need at least ₹5 lakh to invest in them.

7. Certificate Of Deposits

A Certificate of Deposits (also known as a CD) is a negotiable money market instrument – more like a promissory note. A CD’s rates, terms, and amounts vary from institution to institution.

CDs are not supposed to trade publicly and neither they are traded on any exchange.

As a general practice, institutions issue certificates of deposit at a discount on their face value. Banks and financial institutions can issue CDs on a floating rate basis. CDs are directly issued by financial institutions for a minimum deposit of ₹1 lakh and in subsequent multiples.

8. Money Market Mutual Funds

Money Market Mutual Funds are Open-ended fund schemes that tend to snack on a pool of short-term debt securities. They operate like equity Mutual funds that snack on bundles of stocks.

Money Market Funds are short-term debt funds.

The money market mutual funds were introduced by the Reserve Bank Of India (RBI) in the year 1992 and since the year 2000, they are brought under the regulation of the Securities and Exchange Board of India (SEBI).

These funds invest in various money market instruments and aim to offer good returns over up to one year while maintaining high levels of liquidity. The average maturity of a Money Market Fund is one year.

These funds are usually preferred by investors who tend to park their surplus money for short-term goals, risks, and emergencies. A small percentage of investors also utilize money market funds as a holding place for their cash while they look for possibilities in other asset classes like stocks, gold, or real estate.

9. Fixed Deposits

A Fixed Deposit is a safe financial instrument that is offered by most Banks as a fixed-income alternative. A fixed deposit provides a slightly higher rate of interest than a regular savings account. In India, fixed deposits have been the most preferred instrument to save money for rainy days.

☑ They are safe (Up to ₹5 Lakh per bank)

☑ They offer the highest stability as returns are fixed

☑ They can be used for periodic interest payouts

☑ They are not affected by market fluctuations

☑ Some financiers (small banks) also offer higher FD interest rates

Fixed Deposits are now insured under DICGC. Deposit Insurance and Credit Guarantee Corporation (DICGC), is a wholly-owned subsidiary of the Reserve Bank of India (RBI).

DICGC provides deposit insurance that works as a protection cover for bank deposit holders when the bank fails to pay its depositors.

Each depositor’s deposit in a bank is insured up to a maximum of ₹5 lakh, for both principal and interest.

10. Debt Mutual Funds

A Debt Mutual Fund is a scheme that invests in fixed-income instruments, such as Corporate and Government Bonds, corporate debt securities, money market instruments, etc. that offer capital appreciation. They are slightly different from Money Market Funds as they tend to invest money in Bond markets.

These are the long-term Corporate and Government bonds.

Debt funds are also referred to as Fixed Income Funds or Bond Funds.

A few major advantages of investing in debt funds are a low-cost structure (expense ratio), relatively stable returns, fairly high liquidity, and reasonable safety. For investors who want a steady stream of income but are risk-averse, debt funds are suitable. Debt funds are less riskier than equity funds since they are less volatile.

Conclusion

Money markets are an essential part of any economic system because they guarantee the quick and sufficient movement of money. They are also seen as an essential part of any successful investment portfolio to ensure fixed income. For people who want to invest but have a reduced risk tolerance, fixed-income instruments are one of the finest possibilities because they produce constant income.

For a small fee, self-directed investors can gain access to the majority of money market assets that are not immediately available through passive instruments like Money Market Mutual Funds (MMMF) or Debt Mutual funds. There are various benefits to being exposed to debt, including simplicity of use, regular income, tax efficiency, and high liquidity.

Note – Please see a licensed (fee-only) financial counselor for more information; this is not investment advice.

🔔 Investing is expensive, but leaving comments on this blog is free!