Your credit score plays a pivotal role in shaping your access to loans, mortgages, and credit cards. Within this article, we’ll learn some practical tips and strategies designed to assist you in enhancing your credit score and upholding a solid credit history.

The Context

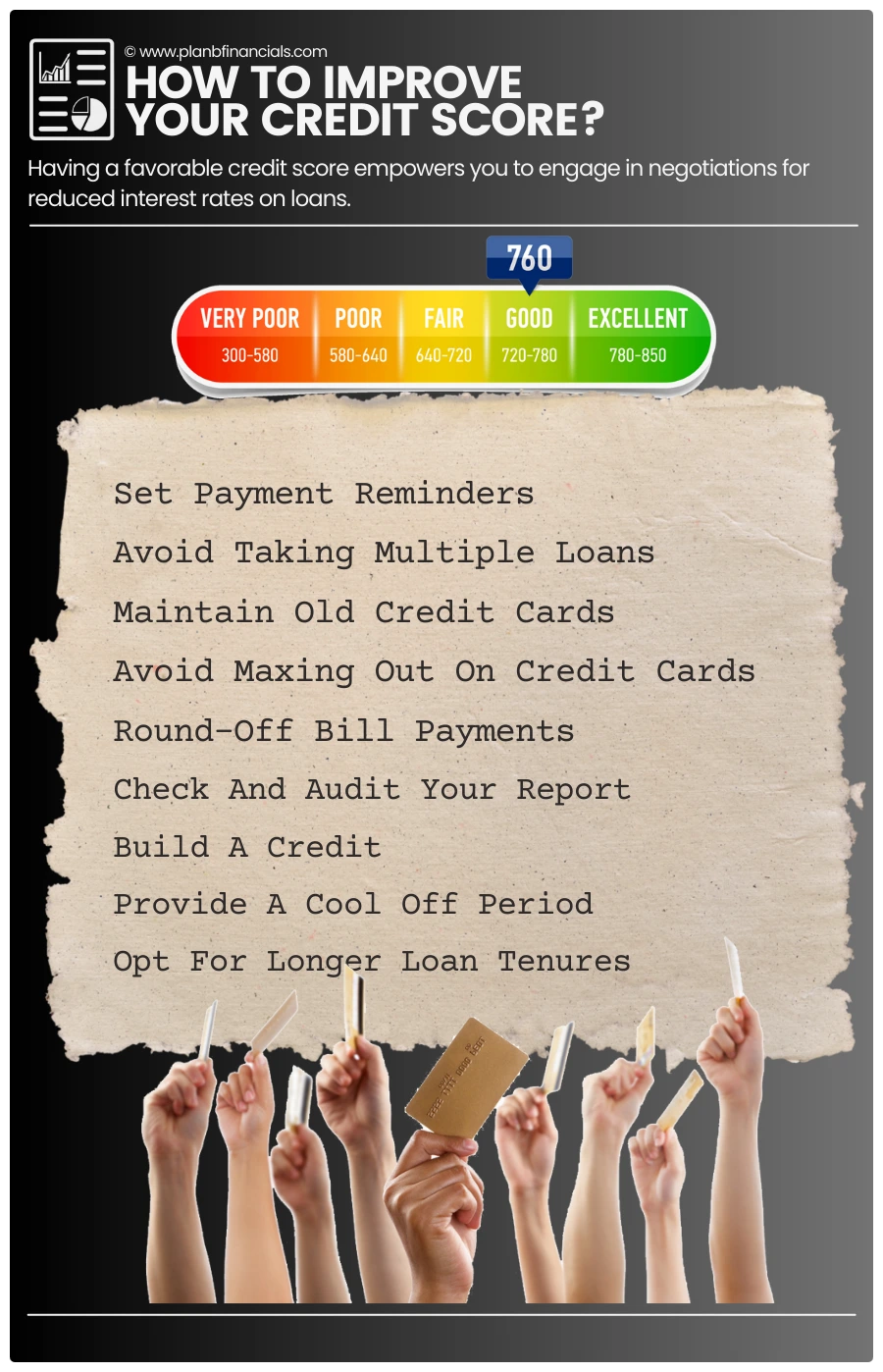

A good credit score gives you the power to negotiate a lower interest rate on leverage money — PlanB

Since the early 1900s, numerous subjective and objective techniques have been used around the world to determine a person’s ability to repay loans and debts. The legacy models were first used by store owners to give credit for the items consumers had purchased.

As these systems evolved through the 1950s, a more developed version called the FICO score was introduced in 1989 by FICO, then called Fair, Isaac, & Company of the U.S.

The great majority of banks and credit grantors currently employ the FICO model, which is based on consumer credit files from the three legitimate national credit agencies Experian, Equifax, and TransUnion.

What Is A Credit Score?

A credit score (also known as CIBIL score in India) is an indicator of a person’s creditworthiness, or their ability to repay debt. It is usually expressed as a number based on the person’s repayment history and credit files across different loan types and credit institutions. A credit score is also known as a credit rating. It’s a three-digit number rating system that ranges between 300–and 850 in the U.S.

The higher the score, the better a borrower looks to potential lenders. In India, it’s also known as the CIBIL TransUnion score and ranges from 300 to 900. The closer your score is to 900, the better your credit rating is. The Credit Information Bureau (India) Limited (CIBIL) is the most popular of the four credit information companies licensed by the Reserve Bank of India.

The other 3 companies are Equifax, High Mark, and Experian. In India, the CIBIL Scoring system was implemented much later—in 2007—to monitor the activities of high-risk borrowers.

Typically a credit score of 800 and above is considered excellent in both India and the U.S.

Because it illustrates how trustworthy or risky you are as a borrower, your credit score is an important metric in the financial world.

Negative information about defaults typically remains on credit records for 7 years.

According to CIBIL and Equifax data, depending on the kind of bankruptcy, insolvency, and bankruptcy remain on your credit report for 7 to 10 years. Your Equifax credit report may contain closed accounts that were paid in full for up to ten years.

The main components that determine your credit score are:

🖱 Your income

🖱 Your existing debts

🖱 Your past credit payments

🖱 Any defaults and delays in payments

🖱 Rejections on loans applied for

There are however provisions to procure no-objection certificates from the lenders in case of any disputes to clear out ‘thy’ name.

The unavoidable use of debt

Many people incur debt to simply survive and meet their families’ most basic necessities for food and shelter.

Some people also seek pleasure in debt to satisfy their need for immediate gratification.

Only a select few, who have the mindsets of investment and financial growth, may take advantage of this system as leverage.

Leverage is a strategy of using borrowed money to increase your returns on investments.

If the net returns on the total money invested in security are higher than the interest you pay on the borrowed funds, you can pocket significant returns.

When utilized wisely, leveraged loans are nice for:

🖱 Purchasing Real Estate (Cash flow kind)

🖱 Stocks (Margins)

🖱 Commodities (Futures)

🖱 Forex Trading (Most common)

🖱 Consumer Leverage (Credits)

Debt that benefits and debt that burdens

There are two types of debt; Bad debt and the Good debt

✓ Bad Debt

The bad type of debt from a consumer’s viewpoint refers to credit, usually used to satiate materialistic needs. This debt type has to do little to improve your net financial outcome in the long run.

Some examples of bad debt are credit card loans, auto loans, personal loans & payday loan advances.

✓ Good Debt

Good debt is specified as money owed for things that can help build wealth or boost income over time. Some examples of good debt are taking out a home loan (mortgage), buying things that save you time and money, buying essential items, and investing in yourself by borrowing student loans.

Good debt may put you in a hole in your net worth initially, but you’ll be better off in the long run for having borrowed the money.

How to Improve your credit score

Here are some ways of improving and maintaining a healthy credit score.

☑ Set Reminders

The most spectacular things in life are the little things. Making a list of regular payments and setting reminders for the due dates is a good idea.

Maintaining and raising a decent credit score requires discipline and “clocking practice“.

☑ Avoid Multiple Loans

It’s the dose that makes the poison. Indulging in too many loans at once projects you as a credit-hungry consumer.

This forces lenders to either reject your application or allow it at a higher interest rate because you signal through your desperate actions an inclination to submit to the terms.

☑ Loyalty Has Its Perks

It would not be a good idea to frequently accept fresh credit card and personal loan offers from rival institutions. You should always make an effort to hold onto your previous credit cards.

Your ability to build a clean data trail for improved credibility and consequently good rating increases if you make on-time payments on your older credit accounts. In most cases, it won’t harm your credit score if you don’t use your old, active credit cards.

☑ Never Cross The Line

Maxing out your credit limit impacts your credit utilization ratio. A credit usage ratio is the ratio of the debt on your credit card to the credit line on that card or the sum of your balances to your combined credit limit.

Talk to your credit card provider about capping your ceiling as you raise the credit limits on the card to make sure you never go over the maximum.

☑ Stay Positive-Negative

The game of positive and negative numbers governs personal money. Always strive to round up your utility bills positively (on the higher side).

Rounding up your bill payments by a few pennies or cents guarantees that you remain current on your payments until the next billing cycle. A negative balance on your statements will imply that the utility providers and lending institutions owe you some cents.

You should be glad that this negative balance does not unfavorably affect your credit score. Your credit score will benefit from this since it shows that you have a credit-healthy balance that automatically adjusts with each new billing cycle.

☑ Review Your Reports

How often do you audit your credit report? Your credit report is created from a variety of bottom-up inputs that pass through numerous billers and point-of-sale machines.

Errors do occur when accounting and reporting variables aren’t very efficient. It is wise to regularly review your credit reports for any obvious errors.

Any mistakes you find must be fixed by bringing up issues with the issuing agencies. This action is also known as the “advance dispute approach“.

☑ Leave Deliberate Trails

This is a tricky one yet useful for the millennials who are just starting their financial journey.

Due to the widespread usage of student loans in the US, an individual credit stream (credit trail) begins earlier than it does in India.

If you have not taken credit in the past, it’s likely, that you will not have a score.

It’s a wise move to purposefully take out affordable credit to establish a solid financial foundation. This makes it easier to get cheap interest rates later in life when the actual struggles start. Loans that you can readily repay without negatively affecting your existing financial status are referred to as having affordable credit.

☑ Doing absolutely nothing

Sometimes maintaining composure in the face of debt can be very effective, especially when trying to repair a damaged credit rating. This method is quite situational, particularly if your credit ratings have already suffered some damage.

Refrain from applying for a new loan for one full financial year while you keep paying EMIs for the existing ones. This will surely help settle the financial books on their own.

☑ Opt For Longer Loan Tenures

Higher-value assets, including real estate, necessitate substantial obligations. Try to opt for longer tenures on big loans.

This ensures a lower EMI that can be managed easily on time and reduces the chances of defaults as life transpires. Besides any excess future cash flows can be diverted into high-yield assets such as stocks and equities.

Conclusion

If used wisely, consumer debt or loans are a terrific method to raise both your CIBIL score and your standard of living. They provide you with the freedom to buy things “Now” that would need years of patience.

A low CIBIL score restricts your choices and typically requires more capital because you either pay a higher interest rate or are required to put down a larger amount of money. This is done to protect the lenders from the risk that a low CIBIL score poses.

When you borrow money, a higher score on the opposite allows you to haggle for loans with lower interest rates. Last but not least, the key to building wealth is awareness to bifurcate good debt from bad debt.

Please feel free to contribute your thoughts and experiences on this subject.

🔔 Investing is expensive, but leaving comments on this blog is free!